Real estate is one of the most proven paths to long-term wealth. For decades, investors around the world have used property to generate passive income, build equity, and protect their capital against inflation. Yet every year, thousands of beginners enter the market with high expectations and walk away with disappointing results.

The problem is rarely a lack of money. More often, it is a lack of structured thinking.

Most beginner investors fall into the same traps:

- They choose a property based on price alone, ignoring whether anyone actually wants to live or work there.

- They calculate returns using only rental income, forgetting taxes, maintenance, vacancy, and loan costs.

- They expect to see profits within one or two years, not understanding that real estate rewards patience.

- They borrow beyond their comfort zone, and one unexpected expense throws their entire cash flow into the negative.

- They skip legal verification, only to discover disputes or unclear ownership after signing the deal.

This guide is written to fix that gap. Whether you have never bought a property before or are just starting to take real estate seriously, this resource will walk you through every critical dimension – from how returns are actually generated, to how to evaluate a location, calculate true costs, manage financing, understand legal risks, and build a strategy that lasts.

This is not a guide about getting rich quickly. It is a guide about making smart, informed decisions – the kind that build real financial stability over time.

By the end, you will think like an investor, not just a buyer.

What Is Real Estate Investment and How Does It Actually Work?

Real estate investment means purchasing property with the intention of generating a financial return – either through rental income, capital appreciation (the property’s value increasing over time), or both. While that definition is straightforward, what determines whether a property actually performs well is far more nuanced.

A common misconception among beginners is that buying property is inherently safe and profitable. It is not automatically either. A property becomes a good investment only when it performs financially over time, relative to what you paid and what it costs to maintain.

The Core Return Equation

Every real estate investment can be evaluated through a simple lens:

Investment Performance = (Rental Income + Appreciation) minus Total Costs

When income and growth are strong while costs remain controlled, the investment works well. When costs are higher than expected, or income is unstable, returns shrink – even on paper-attractive properties.

A Tale of Two Investors

Consider two investors who each have the same budget and invest in similar-value properties in the same year:

- Investor A chooses a flat in a peripheral area because it is cheaper. The neighbourhood has limited employment, few amenities, and weak transport links.

- Investor B spends slightly more on a property near a developing business district with a new metro line under construction.

Five years later:

- Investor A struggles with tenant gaps, had to reduce rent twice, and the property value has barely moved.

- Investor B has had near-full occupancy, raised rent once, and the property has appreciated by 30%.

This is not a story about luck. It is a story about decision quality. Real estate rewards research, patience, and rational thinking far more than it rewards impulsiveness or following trends.

How Real Estate Actually Generates Wealth

There are three primary mechanisms through which real estate builds wealth:

1. Rental Income

This is the money tenants pay you each month. Rental income is your most direct, predictable return – provided you maintain consistent occupancy. The stability of this income depends heavily on location, property type, and tenant demand in the area.

Managing tenants effectively is just as important as choosing the right property. In many cases, long-term performance improves when investors follow a structured property management approach that aligns with their time availability and investment goals.

2. Capital Appreciation

Over time, properties in strong locations tend to increase in value. This appreciation is driven by population growth, infrastructure development, economic activity, and general demand. Appreciation is a long-term benefit and should not be your only reason to invest – but in the right market, it can significantly multiply your wealth.

3. Equity Buildup

If you have a loan on the property, each monthly payment gradually pays down the principal. Over 15 to 20 years, your tenants are effectively helping you own the property outright. This is a form of forced savings that many investors overlook when calculating total returns.

Types of Real Estate Investment – Which One Is Right for You?

Real estate is not a single asset class. It spans multiple property types, structures, and investment vehicles, each with different return profiles, risks, and management demands. Understanding these differences is essential before choosing where to deploy your capital.

1. Residential Real Estate

Residential properties – houses, apartments, condominiums, and townhouses – are the most popular starting point for beginner investors, and for good reason.

Housing demand is relatively stable in most markets. People always need a place to live, which provides a level of income reliability that commercial real estate cannot always match.

Rental yields on residential properties typically range from 3% to 6% annually, depending on city, neighbourhood, and property type.

Returns are moderate but consistent, making residential investment well-suited for:

- First-time investors who want lower complexity

- Those prioritising steady, predictable monthly income

- Investors planning to hold a property for 10 or more years

The main challenge with residential investment is that margins can be tight. If your loan payment is high and you have a vacancy period, monthly cash flow can go negative quickly.

2. Commercial Real Estate

Commercial properties – office spaces, retail shops, warehouses, and industrial units – can generate significantly higher rental yields, sometimes between 7% and 12%. However, they come with proportionally higher risks.

Commercial tenants are businesses, and their ability to pay rent depends on how well those businesses are performing. During economic downturns, commercial vacancies spike. A retail unit in a struggling high street can sit empty for 6 to 12 months before a new tenant is secured. The leases are often longer (3 to 10 years), which can be an advantage or a disadvantage depending on market conditions.

Commercial investment is generally better suited for:

- Investors with prior real estate experience

- Those with larger capital reserves to absorb vacancy periods

- Investors comfortable with higher-risk, higher-reward dynamics

3. Rental Property as a Strategy

Rental property investment is less a property type and more a mindset. It means purchasing property specifically to earn monthly income, with long-term appreciation as a secondary benefit.

The single most important variable in this strategy is occupancy rate – how consistently the property is rented out. A beautifully renovated flat that sits empty for three months a year will underperform a modest property that is rented 11.5 months out of 12.

Experienced rental investors focus on:

- Areas with strong tenant demand (near universities, hospitals, tech hubs, transport links)

- Properties that are easy to maintain and cost-effective to manage

- Tenant quality and lease length for income stability

4. REITs – Real Estate Without the Property

Real Estate Investment Trusts (REITs) are companies that own, operate, or finance income-generating real estate. They are listed on stock exchanges, making them as easy to buy as a share of stock.

REITs are suitable for investors who:

- Want liquidity – REITs can be sold quickly, unlike physical property

- Want exposure to real estate returns without managing physical property

- Have limited capital and cannot afford a down payment

The trade-off is control. REIT returns are influenced by broader market conditions, dividend policies, and management decisions you have no say in. They are better used as part of a diversified portfolio than as a standalone real estate strategy.

5. Real Estate Crowdfunding

Crowdfunding platforms pool money from multiple investors to fund large real estate projects – typically commercial developments, residential complexes, or land acquisitions. This lowers the entry barrier and allows investors to spread their capital across multiple opportunities.

However, this model comes with its own set of risks. Platform credibility, project execution, and regulatory compliance all play a critical role in determining returns. Many beginners underestimate the legal side, even though it directly affects investor protection and capital security.

Before investing, it is important to understand the legal aspects of real estate crowdfunding, including how funds are structured, what rights investors have, and what risks are involved if a project fails.

| Investment Type | Typical Yield | Risk Level | Management Required | Best For |

|---|---|---|---|---|

| Residential | 3–6% | Low–Medium | Moderate | Beginners |

| Commercial | 7–12% | Medium–High | High | Experienced investors |

| REITs | 4–8% | Market-dependent | None | Passive investors |

| Crowdfunding | 6–10% | Medium–High | None | Supplementary use |

| Rental Strategy | Varies | Medium | Moderate | Income-focused buyers |

How to Start Real Estate Investment – A Step-by-Step Framework

Starting without a process is one of the most costly mistakes a new investor can make.

The following framework gives you a structured approach that reduces emotion and improves the quality of every decision.

Step 1: Clarify Your Financial Position

Before you look at a single property listing, you need an honest picture of your finances. This goes beyond knowing how much you have saved – it means understanding your total capacity and your tolerance for financial pressure.

Key questions to answer:

- What is your total available capital? (savings, liquid assets)

- How much can you borrow, and at what monthly repayment?

- Do you have 6 to 12 months of emergency reserves separate from your investment capital?

- Can you cover negative cash flow for 2 to 3 months if the property sits vacant?

- What is the maximum monthly loss you can absorb without financial stress?

A disciplined investor always stress-tests the worst case: What happens if the property is empty for four months? What if a major repair is needed in year one? If the investment only works under perfect conditions, it is too risky.

Step 2: Define Your Investment Goals

Different goals require different strategies. Be specific about what you want before you start searching:

- Are you investing for monthly income now, or long-term wealth 10 to 20 years from now?

- Do you want to manage the property yourself or hire a property manager?

- Are you looking for one property to start, or building toward a multi-property portfolio?

- What is your target holding period – 5 years, 10 years, or indefinitely?

Your answers will directly shape which property type, location, and financing structure is right for you.

Step 3: Conduct Thorough Market Research

Location drives the majority of real estate performance. Markets are not uniform – within a single city, one neighbourhood can have 95% occupancy while another has 70%. Research should be data-driven, not based on gut feel or hearsay.

Factors to analyse:

- Price trends over the past 3 to 5 years — is the market rising, flat, or declining?

- Rental vacancy rates — what percentage of properties in the area are unoccupied?

- Infrastructure and development pipeline — are new roads, metro lines, or commercial zones planned nearby?

- Employment growth — is the area attracting new jobs and businesses?

- Population trends — is the neighbourhood growing or shrinking?

| Research Factor | Why It Matters | Where to Find It |

|---|---|---|

| Price trends | Indicates appreciation potential | Property portals, government records |

| Vacancy rates | Predicts income stability | Local estate agents, housing data |

| Infrastructure plans | Future demand driver | City development plans, news |

| Employment growth | Tenant pool quality | Economic reports, company announcements |

| Population trends | Long-term demand | Census data, municipal records |

Working with experienced professionals can also improve decision quality. Understanding how real estate professionals earn gives you better insight into how agents operate, negotiate, and prioritise deals in different market conditions.

Step 4: Evaluate Location Using the PCTS Framework

Once you have shortlisted areas, evaluate each location systematically using four criteria:

- Proximity

Distance to employment centres, business districts, educational institutions, and hospitals. - Connectivity

Quality of transport infrastructure — metro, buses, highways, and walkability scores. - Completeness

Availability of everyday amenities — supermarkets, schools, healthcare, and entertainment. - Trajectory

Planned future development and the direction the area is heading over 5 to 10 years.

A location that scores well across all four dimensions has the strongest foundation for sustained rental demand and price appreciation.

Step 5: Select and Evaluate Individual Properties

Once your location is confirmed, narrow down to specific properties. Compare each against three criteria:

- Price vs. market value

Is the asking price in line with comparable sales in the area? Is there room to negotiate? - Rental yield potential

Based on local rents, what monthly income can you realistically expect? - Condition and hidden costs

What repairs or upgrades are needed before tenanting? How old are the electrical systems, plumbing, and roof?

The best investment is not always the newest or most aesthetically appealing property. It is the one offering the best return relative to its total acquisition and operating cost.

Step 6: Get Professional Verification

Before making any offer, always engage a structural inspector and a legal professional. Do not skip this step to save money. A property with undisclosed structural issues or a disputed title can cost you far more than any professional fee.

Understanding the True Cost of Real Estate Investment

One of the most common reasons beginners are disappointed by their returns is that they only account for the purchase price. The full cost of a real estate investment is always higher – sometimes significantly so.

Acquisition Costs

These are the costs you pay when purchasing the property:

- Down payment: 10%–25% of property value, based on lender and loan type.

- Stamp duty & registration: 1%–8%, depending on location.

- Legal fees: 0.5%–1.5% for documentation and verification.

- Inspection fees: Cost for structural and pest checks.

- Brokerage/commission: 1%–3% of the property price, if applicable.

Understanding acquisition costs upfront ensures you don’t underestimate your initial investment or distort your return expectations from day one.

Financing Costs

If you are using a loan – which most investors do – these ongoing costs directly affect your cash flow:

- Monthly loan repayment: Principal + interest, which must be compared directly against rental income.

- Loan processing fees: One-time charges by the bank or lender at the time of loan approval.

- Prepayment or exit penalties: Some loans charge a fee if you sell or refinance before a specified period.

Financing decisions should be evaluated carefully, as even small differences in loan terms can significantly impact long-term cash flow and profitability.

Ongoing Operational Costs

These are the recurring costs of owning and renting out property:

- Property tax: 0.5%–2% of value, paid annually or semi-annually.

- Maintenance & repairs: Around 1% of property value per year.

- Property management: 8%–12% of monthly rent, if hired.

- Insurance: Covers property and landlord risks.

- Vacancy utilities: Basic costs even when the property is empty.

Consistent profitability depends not just on income, but on how efficiently you manage and control ongoing operational expenses.

Hidden Costs That Erode Returns

These are the costs most beginners fail to include in their calculations:

- Vacancy loss: Empty months reduce income; even 90% occupancy means ~36 days vacant yearly.

- Pre-rental renovation: Basic upgrades like paint, flooring, and fixtures before leasing.

- Tenant turnover: Cleaning, minor fixes, and listing costs after a tenant leaves.

- Major repairs: Big costs like roof, plumbing, or electrical issues over time.

The difference between a good investment and a poor one often lies in how well you anticipate and account for these hidden costs.

Case Example: A property generates $1,400/month in rent. In Year 1, it sits vacant for 2.5 months and requires $3,200 in repairs. Actual income: $16,800 minus $3,200 = $13,600 — nearly 19% below projections. This is why buffer planning is non-negotiable.

Taxes are another area where many beginners make incorrect assumptions. Before finalising your cost estimates, it’s important to understand the difference between real estate taxes and property taxes , as they can affect your long-term returns more than expected.

| Cost Category | Typical Range | One-Time or Ongoing |

|---|---|---|

| Down payment | 10%–25% of value | One-time |

| Stamp duty / registration | 1%–8% of value | One-time |

| Legal fees | 0.5%–1.5% of value | One-time |

| Property tax | 0.5%–2% of value/yr | Ongoing (annual) |

| Maintenance | 1% of value/yr | Ongoing |

| Property management | 8%–12% of rent | Ongoing (annual) |

| Vacancy loss | Varies (budget 8–10%) | Ongoing |

| Insurance | Varies by property | Ongoing (annual) |

Financing Options and Loan Strategy

Most real estate investments are partially financed through loans. Used wisely, leverage amplifies your returns. Used poorly, it becomes the largest source of financial risk in your investment.

1. Home Loans / Residential Mortgages

These are standard bank loans for purchasing residential property. They typically offer the most competitive interest rates and the longest repayment terms (15 to 30 years). They are the most accessible option for first-time investors.

2. Investment Property Loans

Some banks offer loans specifically for investment properties, which may carry slightly higher interest rates than owner-occupier loans, since lenders view investment properties as higher risk. Requirements may include a higher down payment (typically 20% to 30%).

3. Construction Loans

If you are building rather than buying, construction loans disburse funds in stages as building milestones are completed. They typically convert to a standard mortgage after construction is finished. These carry more complexity and short-term interest-only payments.

Because of this staged structure, many investors miscalculate their actual borrowing cost and repayment timeline. Before choosing this route, it is important to understand how construction loan calculations work, especially how interest is applied during different phases of construction.

Key Metrics to Evaluate Before Taking a Loan

- Loan-to-Value Ratio (LTV)

The loan amount as a percentage of the property value. Lower LTV means less risk. Most lenders cap at 80% LTV for investment properties. - Interest rate

Fixed vs. floating. Fixed rates provide repayment certainty; floating rates may start lower but carry the risk of rising over time. - Loan tenure

Longer tenure means lower monthly payments but higher total interest paid. Shorter tenure means higher payments but you build equity faster. - Debt Service Coverage Ratio (DSCR)

Rental income divided by total loan repayment. A DSCR above 1.2 is generally considered healthy.

The Golden Rule of Real Estate Financing

Your monthly loan repayment should ideally not exceed 70–80% of your expected monthly rental income. This leaves a buffer for operational costs, maintenance, and vacancy periods. If the loan payment exceeds rental income, you need to cover the gap from personal income – and this gap will compound over time.

Fixed vs. Floating Rate – A Simple Comparison

| Factor | Fixed Rate | Floating Rate |

|---|---|---|

| Monthly payment | Predictable | Can change over time |

| Initial rate | Usually higher | Usually lower to start |

| Risk | Locked in if rates drop | Exposed if rates rise |

| Best for | Conservative investors | Short-term holders or rate-savvy investors |

ROI, Cash Flow, and Profit Analysis

Understanding returns before you buy is fundamental. Too many investors discover what they actually earned only after years in the market. Here is how to calculate it properly beforehand.

1. Gross Rental Yield

This is the starting point for comparing properties. It tells you how much income the property generates relative to its value, before any expenses.

Gross Rental Yield = (Annual Rental Income / Property Value) x 100

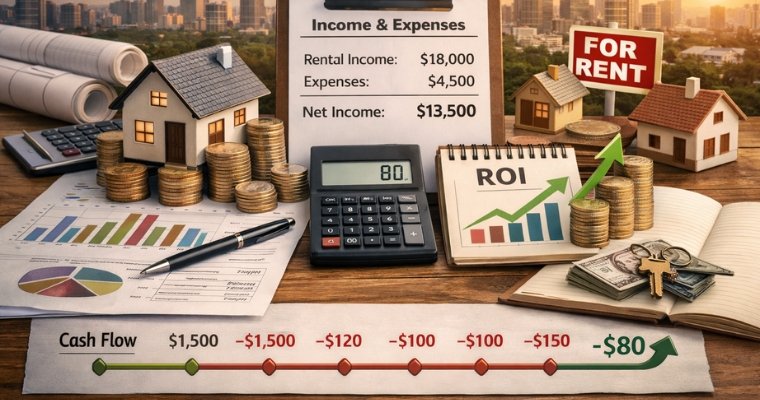

Example: A property worth $280,000 that rents for $1,500/month generates $18,000 annually. Gross yield = (18,000 / 280,000) x 100 = 6.4%.

2. Net Rental Yield

This is the more meaningful number. It accounts for your actual operating expenses:

Net Rental Yield = ((Annual Rent minus Annual Expenses) / Property Value) x 100

If your expenses total $4,500 per year, net income is $13,500. Net yield = (13,500 / 280,000) x 100 = 4.8%.

3. Cash Flow Analysis

Cash flow is the money left in your pocket after every expense – including the loan – has been paid. It is the most important number for day-to-day financial sustainability.

| Component | Monthly Amount |

|---|---|

| Gross rent received | $1,500 |

| Loan repayment | – $1,500 |

| Property tax (monthly) | – $120 |

| Maintenance reserve | – $100 |

| Management fee (10%) | – $150 |

| Net monthly cash flow | $80 |

A positive cash flow means the investment is self-sustaining. A negative cash flow is not automatically disqualifying – if appreciation is strong and you can afford the gap – but it adds financial pressure that must be planned for explicitly.

4. Return on Investment (ROI)

ROI = (Net Annual Profit / Total Capital Invested) x 100

Total capital invested includes down payment + all acquisition costs + any renovation spend. This gives you the true return on your equity deployed.

5. Total Return Over Time

The full picture of real estate returns combines three elements:

- Cash yield. Annual net cash flow as a percentage of capital invested.

- Appreciation gain. The increase in property value over the holding period.

- Equity buildup. The reduction in loan principal paid down by rental income over time.

A combined annual return of 8% to 12% – across all three elements – is generally considered a strong real estate investment in most markets.

Real Estate Investment Risks and How to Manage Them

Every investment carries risk. Real estate is no exception. The difference between investors who succeed and those who struggle is not the absence of risk – it is their ability to identify, plan for, and manage it.

The Major Risk Categories

- Location Risk

Choosing a location that lacks demand is the single biggest mistake in real estate. A poor location means weak rents, frequent vacancies, and minimal appreciation. Unlike other risks, location risk is almost impossible to fix after you have bought – you cannot move the property. - Vacancy Risk

Every unoccupied day is lost income. Vacancy can result from poor location, overpriced rent, a declining local economy, or simply bad luck with timing. Investors should always model their returns assuming 8% to 10% vacancy – roughly one month per year. - Interest Rate Risk

If you have a floating rate loan, rising interest rates increase your monthly payment without any corresponding increase in rental income. Even a 1% rise in rates can significantly reduce cash flow on a leveraged property. - Legal and Title Risk

Purchasing a property with a disputed title, pending litigation, or unapproved construction can result in financial loss, legal complications, or the inability to sell. This risk is entirely avoidable through proper due diligence. - Maintenance and Structural Risk

Older properties or poorly inspected ones can reveal costly structural issues after purchase. A single major repair—roof, foundation, plumbing—can wipe out a full year of net income. In addition to structural issues, investors should also be aware of on-site risks during construction or renovation phases. Problems like material theft or site damage can delay projects and increase costs. Understanding construction-related risks and theft prevention helps reduce these avoidable losses. - Tenant Risk

Problem tenants who do not pay on time, damage the property, or require costly eviction proceedings can significantly affect returns. Good tenant screening upfront dramatically reduces this risk.

Common Beginner Mistakes – and How to Avoid Them

| Mistake | Why It Happens | How to Avoid It |

|---|---|---|

| Buying on emotion | Property ‘feels right’ | Use data and calculations, not feelings |

| Skipping inspection | Trying to save on fees | Always get a structural survey |

| Ignoring total costs | Only see purchase price | Build a full cost model before buying |

| Overleveraging | Wanting a bigger property | Keep DSCR above 1.2 |

| Expecting quick profits | Unrealistic timelines | Plan for a 7-10 year horizon |

| No emergency fund | Underestimating variability | Reserve 3-6 months of expenses |

| Skipping legal checks | Trusting the seller | Always verify title independently |

Tenant Management and Property Operations

Owning a property is only half the work. Managing it well – specifically finding and retaining good tenants – determines whether your investment generates steady income or becomes a source of constant stress.

Finding Quality Tenants

Quality tenants pay on time, respect the property, and stay longer. Finding them requires a structured screening process, not just accepting the first applicant.

A solid tenant screening process includes:

- Income verification

The tenant’s monthly income should be at least 3x the monthly rent. - Employment stability

Prefer tenants in stable, long-term employment over those with short contracts. - References

Request references from previous landlords and verify them by calling directly. - Credit check

In markets where this is accessible, a credit check reveals payment history. - Background check

For higher-value properties, a basic background check reduces risk.

Setting the Right Rent

Overpricing your rent leads to extended vacancy. Underpricing reduces your returns unnecessarily. Research comparable rentals in your micro-location – ideally within a 500-metre radius – to understand the market rate.

A small discount from the top of the market often pays for itself by reducing tenant turnover and vacancy periods.

DIY Management vs. Hiring a Property Manager

Managing a property yourself saves on fees but requires time, availability, and knowledge of landlord-tenant law. A property manager typically charges 8% to 12% of monthly rent but handles tenant queries, maintenance coordination, rent collection, and legal compliance.

If you live far from the property, own multiple units, or simply prefer a passive role, a professional manager often pays for itself in time saved and problems prevented.

Lease Agreements

Always use a formal written lease agreement, reviewed by a legal professional. The lease should clearly specify:

- Rent amount and payment due date

- Lease duration and renewal terms

- Maintenance responsibilities (what the landlord covers vs. the tenant)

- Conditions for security deposit return

- Notice periods for termination

Tax Implications of Real Estate Investment

Tax is one of the most consistently underestimated costs in real estate investment. Understanding your obligations – and the deductions available to you – directly affects your net return.

Rental Income Tax

In most jurisdictions, rental income is treated as taxable income. It is added to your total income and taxed at your applicable marginal rate. The exact rate and structure depends on local tax law.

However, many expenses are deductible against rental income, which can significantly reduce your tax liability:

- Mortgage interest payments

- Property management fees

- Maintenance and repair costs

- Insurance premiums

- Depreciation of the building and fixtures (in many jurisdictions)

- Professional fees – accountant, lawyer, property inspector

Capital Gains Tax

When you sell a property for more than you paid, the profit is typically subject to capital gains tax. The rate varies significantly by country and holding period. In many jurisdictions, properties held for longer periods are taxed at a lower rate – which is another reason to think long-term.

Stamp Duty and Transaction Taxes

Most countries impose a transaction tax when property changes hands. This is typically paid by the buyer and ranges from 1% to 10%+ depending on the jurisdiction, property value, and whether the buyer already owns property.

Always consult a qualified tax advisor in your specific jurisdiction before making investment decisions. Tax rules change, vary by location, and can have a material impact on your net returns.

Legal Verification and Documentation Checklist

Legal due diligence is non-negotiable. A property that appears perfect can become a financial nightmare if the ownership history is unclear, there are pending court cases, or required approvals were never obtained.

Ownership Verification

The most basic check: confirm that the person selling the property is the legal owner, and that ownership is free from disputes, encumbrances, or third-party claims.

Steps to verify ownership:

- Request the original title deed and verify it against official government land records.

- Check for any mortgages, liens, or charges registered against the property.

- Confirm there are no ongoing disputes or legal cases involving the property.

- If the seller is a company, verify the company’s registration and the signatory’s authority to sell.

Document Checklist Before Purchase

| Document | What to Check |

|---|---|

| Title deed | Matches seller’s identity; no encumbrances |

| Sale agreement | Price, terms, conditions – reviewed by a lawyer |

| Property tax receipts | All dues paid up to date; no outstanding liability |

| Building approvals | All floors and structures are officially approved |

| Occupancy certificate | Property is legally authorised for occupation |

| No-objection certificates | Where required – from housing authority, municipality |

| Utility clearances | No outstanding water, electricity, or municipal dues |

| Society / HOA records | No pending maintenance dues from previous owner |

If any document is missing, unclear, or raises questions, do not proceed until you have professional legal advice. A qualified conveyancing lawyer is not an optional cost – they are your protection against potentially permanent financial damage.

Exit Strategies – When and How to Sell

A complete investment strategy includes knowing when and how to exit, not just when to buy. Many investors hold properties beyond their optimal return window simply because they have not planned an exit strategy.

Common Exit Strategies

- Long-Term Hold and Sell. The most common strategy for residential investors. Hold the property for 7 to 15 years, benefit from appreciation and rental income, then sell when the market is strong and your equity is maximised.

- Sell After Renovation. Buy a property that needs work, renovate it, and sell at a higher price. This strategy (often called ‘fix and flip’) requires skill in estimating renovation costs and timing the market. It is higher effort and higher risk than a long-term hold.

- Refinance and Hold. Once a property has appreciated significantly, you can refinance — take a new, larger loan against the increased value — and use the proceeds to fund a second investment while keeping the original property. This is how experienced investors scale their portfolio.

- 1031 Exchange (US-Specific). In the United States, a 1031 exchange allows you to sell an investment property and defer capital gains tax by reinvesting the proceeds into a new property of equal or greater value within a specified period. Equivalent provisions exist in other jurisdictions under different names.

Signs It May Be Time to Sell

- The property’s maintenance costs are consistently rising and eating into returns.

- The local market has peaked and there are early signs of a correction.

- Better opportunities exist elsewhere and your capital would generate higher returns if redeployed.

- Your personal financial situation has changed and you need liquidity.

Calculation Tools and Formulas Every Investor Should Know

Making investment decisions with calculations rather than assumptions leads to consistently better outcomes. Here are the core formulas you should apply before any purchase.

| Formula | Calculation | What It Tells You |

|---|---|---|

| Gross Rental Yield | (Annual Rent / Property Value) x 100 | Basic income return |

| Net Rental Yield | ((Annual Rent minus Expenses) / Property Value) x 100 | Real income after costs |

| Cash Flow | Monthly Rent minus Loan minus All Expenses | Monthly surplus or deficit |

| ROI | (Net Annual Profit / Total Capital Invested) x 100 | Return on your equity |

| DSCR | Monthly Rent / Monthly Loan Payment | Loan safety buffer |

| Payback Period | Total Investment / Annual Net Income | Years to recover capital |

| Cap Rate | (Net Operating Income / Property Value) x 100 | Market-independent yield |

Using a Pre-Purchase Checklist

Before signing on any property, run through this checklist:

- Calculate gross and net rental yield – does it meet your target?

- Model monthly cash flow under 3 scenarios: best case (full occupancy), realistic (90% occupancy), and worst case (70% occupancy).

- Calculate total acquisition cost including all fees, taxes, and initial repairs.

- Verify DSCR – is your rental income at least 1.2x your loan payment?

- Confirm legal documents are in order.

- Get a structural inspection report.

- Research comparable rental rates within 500 metres.

- Confirm your emergency reserve is intact and separate from investment capital.

Frequently Asked Questions

Yes, in markets with strong underlying demand. The key variables are location quality, cost discipline, and a realistic return timeline. Macro factors like interest rates and inflation affect returns, but they affect all asset classes. Real estate remains one of the most reliable long-term wealth-building tools available to individual investors.

At minimum, you need a down payment of 10% to 25% of the property value, plus acquisition costs (typically 3% to 10%), plus an emergency reserve of 3 to 6 months of loan repayments. For a $200,000 property, total starting capital is often $40,000 to $70,000 depending on location and loan terms.

A combined annual return of 6% to 10% – including rental income, appreciation, and equity buildup – is considered reasonable for residential investment. Higher returns are possible with commercial properties or well-timed markets, but come with higher risk.

Yes. Rental property offers the most direct, manageable entry point. It provides regular income that helps offset carrying costs, and residential properties are relatively easier to understand and manage than commercial assets.

Poor location selection, closely followed by underestimating total costs. Both are avoidable through research and disciplined calculation.

A minimum of 5 years is generally needed to recover acquisition costs. A 7 to 10 year hold is where most investors see meaningful appreciation returns. Holding longer, in the right market, typically compounds returns significantly.

Yes, and most investors do. The key is ensuring your rental income is sufficient to cover loan repayments with a comfortable margin. Never borrow based on best-case income projections – always model for realistic and conservative scenarios.

Not necessarily. If you live near the property, are comfortable with tenant communication, and understand local landlord-tenant law, self-management can save significant money. However, for investors who want a more passive role or who own multiple properties, a professional manager is worth the fee.

Use consistent calculations: gross yield, net yield, cash flow, ROI, and DSCR. Apply the same framework to every opportunity and compare them on an equal basis. Avoid making decisions based on aesthetics, price alone, or a seller’s projections without independent verification.

Read also: Real Estate Investment Guidance

Final Thought

Real estate does not reward the lucky. It rewards the disciplined. The investors who build lasting wealth through property are not necessarily the ones with the most capital, the best connections, or the most adventurous risk appetite. They are the ones who make consistent, well-researched decisions – and stick to them through the inevitable fluctuations of the market.

If you apply the frameworks in this guide consistently, real estate can become one of the most reliable pillars of your financial life. The foundation is not capital. It is clarity.

For more in-depth guides on specific topics, visit trustcliq.com. We publish regular, research-backed content on real estate investment, financing, property risk, and buying strategy – designed to help you make better decisions at every stage of your journey.